목표: Bayesian statistical modeling and probabilistic machine learning

방법: advanced Markov chain Monte Carlo and variational fitting algorithms

PyMC3 (a probabilistic programming framework) 설치 명령어 :

conda create -n pymc_env -c conda-forge python libpython mkl-service numba python-graphviz scipy arviz

conda activate pymc_env

pip install pymc3

------------------------------------------------------------------------------------------------------------

Probabilistic Programming (PP)

▪ allows automatic Bayesian inference

▪ on complex, user-defined probabilistic models

▪ utilizing “Markov chain Monte Carlo” (MCMC) sampling

▪ PyMC3

▪ a PP framework

▪ compiles probabilistic programs on-the-fly to C

▪ allows model specification in Python code

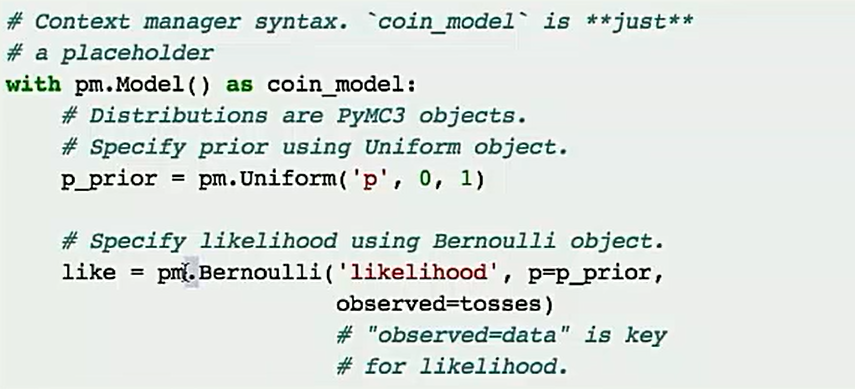

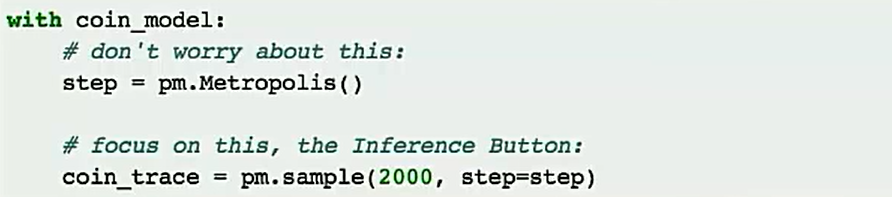

PyMC3:

statistical distributions

sampling algorithms

syntax

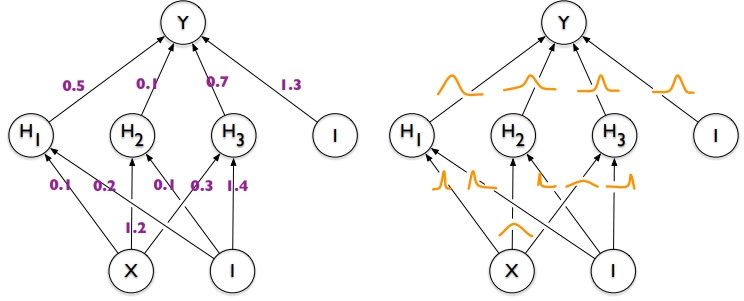

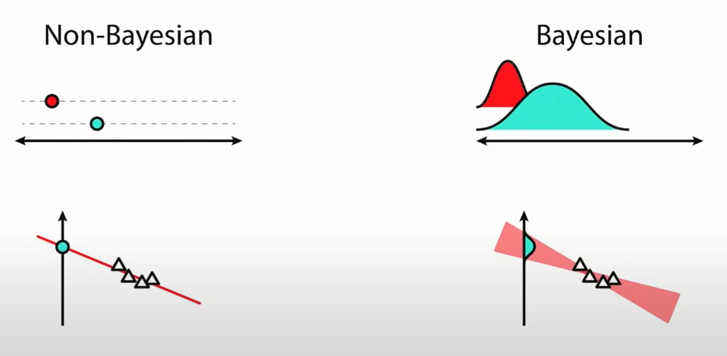

n번 동전을 던져서 h번 앞이 나온경우?

weak prior, strong prior를 가지는 경우를 생각한다.

------------------------------------------------------------------------------------------------------------

Estimating probabilities with Bayesian modelling in python

--------------------------------------------------------------------------------------------------------------

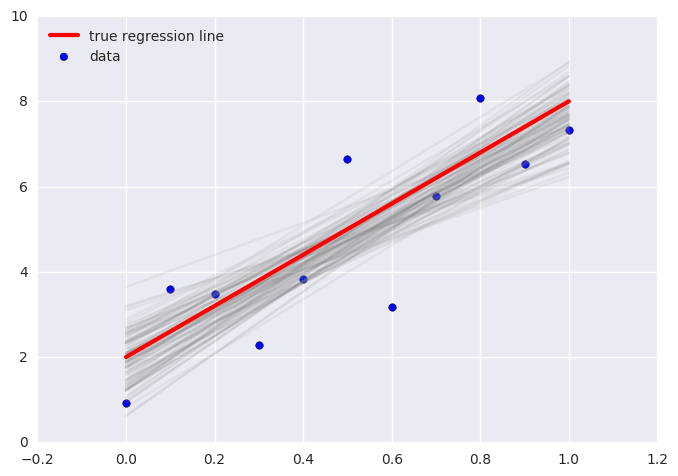

# observed data

np.random.seed(123)

n = 11

_a = 6

_b = 2

x = np.linspace(0, 1, n)

y = _a*x + _b + np.random.randn(n)

niter = 10000

with pm.Model() as linreg:

a = pm.Normal('a', mu=0, sd=100)

b = pm.Normal('b', mu=0, sd=100)

sigma = pm.HalfNormal('sigma', sd=1)

y_est = a*x + b

likelihood = pm.Normal('y', mu=y_est, sd=sigma, observed=y)

trace = pm.sample(niter, random_seed=123)

t = trace[niter//2:]

pm.traceplot(trace, varnames=['a', 'b'])

pass

plt.scatter(x, y, s=30, label='data')

for a_, b_ in zip(t['a'][-100:], t['b'][-100:]):

plt.plot(x, a_*x + b_, c='gray', alpha=0.1)

plt.plot(x, _a*x + _b, label='true regression line', lw=3., c='red')

plt.legend(loc='best')

pass

--------------------------------------------------------------------------------------------------------------

%matplotlib inline

import pymc3 as pm

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

%config InlineBackend.figure_formats = ['retina']

plt.rc('font', size=12)

plt.style.use('seaborn-darkgrid')

# 1. load the stock returns data.

series = pd.read_csv('stock_returns.csv')

returns = series.values[:1000]

# 2. first, let's see if it makes sense to fit a Gaussian distribution to this.

with pm.Model() as model1:

stdev = pm.HalfNormal('stdev', sd=.1)

mu = pm.Normal('mu', mu=0.0, sd=1.)

pm.Normal('returns', mu=mu, sd=stdev, observed=returns)

with model1:

trace = pm.sample(500, tune=1000)

preds = pm.sample_posterior_predictive(trace, samples=500, model=model1)

y = np.reshape(np.mean(preds['returns'], axis=0), [-1])

--------------------------------------------------------------------------------------------------------------Bayesian_Linear_Regression.zip

--------------------------------------------------------------------------------------------------------------

Monte Carlo dropout

--------------------------------------------------------------------------------------------------------------